Introduction

As a manager, every decision you make has financial implications for your company.

You must develop basic financial knowledge to understand how your actions impact the company’s finances, and to effectively advocate for yourself and your team.

Accounting activities can be broadly categorized under two types:

- Financial accounting: What you prepare for outsiders (e.g., tax returns).

- Managerial accounting: What you prepare for yourself (e.g., costing, forecasting).

Although both start with the exact same raw data, the way you track, analyze and visualize finances for your own decision-making can be radically different from what’s required by government regulations.

After all, tax and market authorities are focused on making it easy to understand and compare all types of businesses, whereas your goal is to understand your specific business, or even just a single department or process within it.

We strongly recommend that you outsource financial accounting to a professional bookkeeper and accountant. As such, we will provide only a broad overview of the topic and instead focus on the kind of managerial accounting you will benefit from as a lab manager.

💸 Cash vs Accrual accounting There are two ways of doing your accounts: Cash and Accrual. Throughout this course, we will use Accrual accounting. In Cash accounting, revenue and expenses are recorded at the moment when cash exchanges hands. Small businesses and personal finances mainly use this method. In Accrual accounting, revenue and expenses are recognized when they occur. A purchase occurring in June is recorded in June, even if you don’t pay for it until August. Accrual accounting gives a more accurate view of the company’s health. More importantly, all companies with a broad base of shareholders or creditors are required to follow accrual accounting under both US Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS).

Financial accounting

There are three types of financial statements you need to familiarize yourself with to gain a basic understanding of your company’s finances:

- Balance sheet

- Profit and loss statement

- Cash flow statement

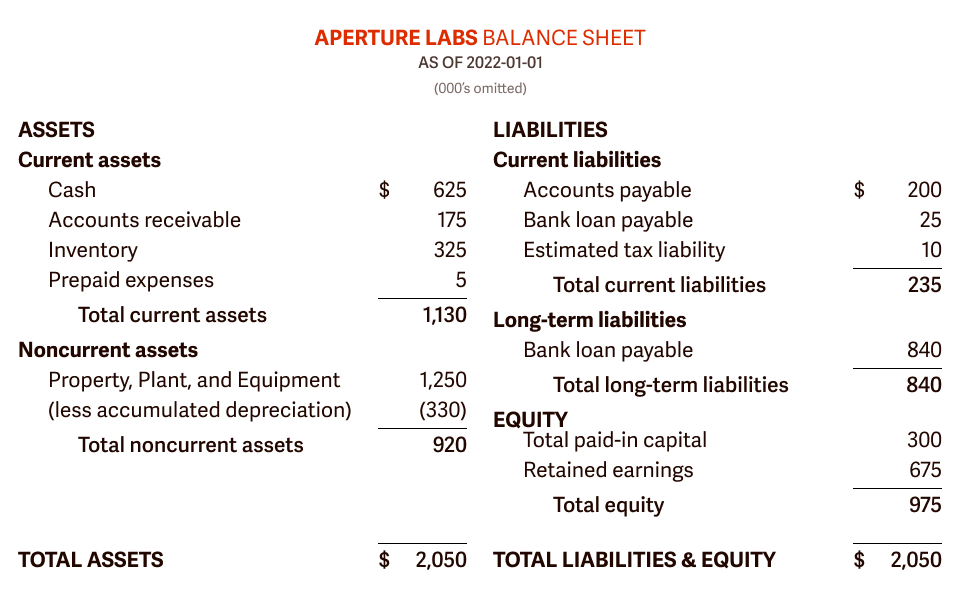

Balance sheet

Below is an example balance sheet for Aperture Labs. It provides a quick snapshot of the company’s health, priorities and composition.

🔢 Financial formatting Notice how negative numbers in accounting are wrapped in parentheses instead of being prepended with a minus. This makes them easier to spot and read. You can easily achieve this in Excel by changing a column’s formatting from Text to Accounting.

Assets are items that are owned and controlled by the company, valuable to the company, and acquired at a measurable cost.

Cash, inventory, investments and property are examples of assets, while employees are not (the company does not control them, and they were not purchased at a cost).

Liabilities are debts owed to a third party in return for borrowed goods, services, or monies.

Some examples include accounts payable, loans payable and taxes. This could be the money you owe to your bank, inventory supplier, or a lab appliance company (if you purchased equipment on credit).

Finally, Equity is money either supplied by investors (founders, VCs, angels, etc.) or generated from profitable operations (such as retained earnings).

🪙 Double-entry accounting Balance sheets are based on the accounting equation: Assets = Liabilities + Equity. As a result, every transaction requires two entries, but the two are not always in the same place. If you purchased a fridge on credit, you’d acquire an Asset (Equipment) and create a Liability (Accounts Payable). On the other hand, if you bought a bottle of emulsifier with cash, you’d reduce one Asset (Cash) and increase another Asset (Inventory), yet your Liabilities would remain unchanged.

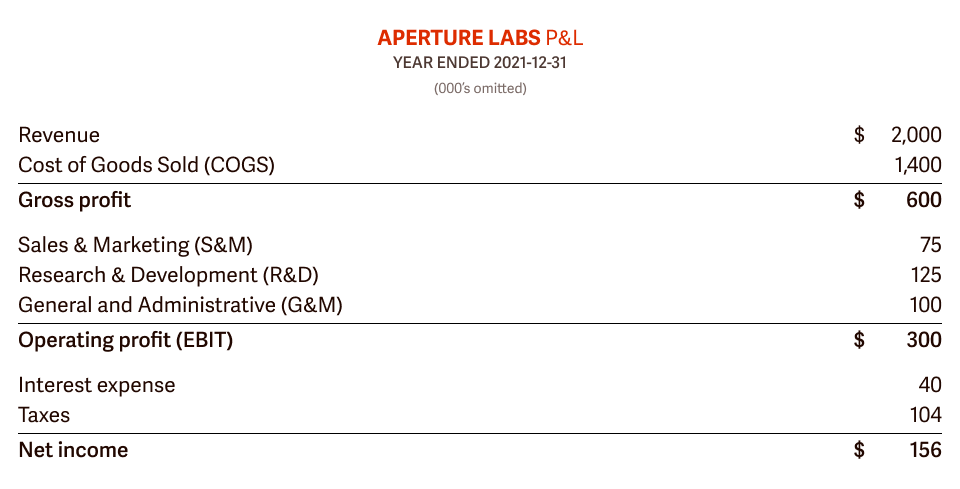

Profit and loss statement

Also called an income statement, the P&L is used to calculate the Net Income by subtracting Expenses from Revenues (both notably absent on the balance sheet).

If the balance sheet is a snapshot of what your company owns and owes at one point (its financial position), the P&L statement is a film of its revenues and expenses over a period of time (its financial performance).

🌍 The Tower of Babel of accounting Accounting is unfortunately ripe with terminology that is not just confusing but also inconsistent even within a single country. For example, Net Income is also known as Net Profits, or Net Earnings. Things get even hairier once you need to communicate across borders — Revenue in North America is often called Turnover in Europe, Asia-Pacific, or the UK, while the latter term describes replacing employees in the US.

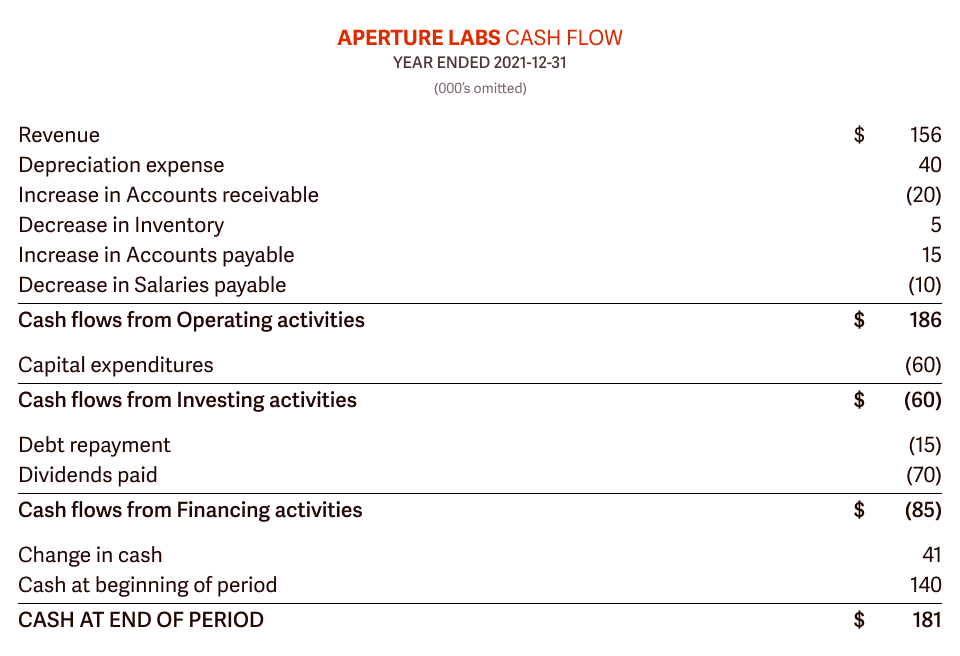

Cash flow statement

As we’ve seen, in Accrual accounting, revenues and expenses don’t necessarily equal cash inflows and outflows, so you could potentially run out of cash even if your net income is in the black.

A Cash Flow Statement (CFS) is the place to check whether your business is viable in the short term, and whether you’ll be able to pay any upcoming bills.

Above, you can see how cash has moved in and out of Aperture Labs as a result of three types of activities:

- Operating: Cash generated from/spent on the company’s products and services (including taxes).

- Investing: Cash from the purchase or sale of equipment, loans from customers or to vendors, etc.

- Financing: Cash from banks or investors, payments of dividends, stock repurchases, etc.

Going deeper

We could run an entire course (or two, or three) on how to prepare these statements and the intricacies of each entry, but the above should be enough for you to quickly assess the finances of your lab based on the documents prepared by your accountant.

If you’d like to dig deeper, such as into the difference between current and noncurrent assets, depreciation, amortization, how to write-off expired inventory, or how to calculate the cost of goods sold, we’ve included links to additional resources at the end.

Managerial accounting

Financial accounting, which we covered in the previous section, was focused on presenting company-level, historical data to external stakeholders, following defined reporting standards.

Managerial accounting is almost the opposite. It is prepared for company insiders in a way that works best for your particular needs, it can include future projections, and it often reports on individual departments and projects.

Capital budgeting

As an individual researcher, buying a fancy new spectrometer is always a good idea and something you might have actively fought for in the past.

As a manager, you need to carefully analyze such investments and their financial impact on the business.

Payback period

One question you might want to ask yourself is ‘How soon will the microscope pay for itself?’, or the payback period of the item.

For example, a $3,000 spectrometer that saves $1,000 in outsourcing costs every year, the payback period is $3,000/$1,000 = 3 years.

Make sure to account for the service life of the equipmen. If you’re buying equipment with a payback period of 7 years, but a lifespan of 5, it should not be purchased!

⌛ Time value of money The payback period calculation is a good start, but it ignores that the value of $1,000 today is higher than if you receive it in the future (as you could invest and grow it in value over the years). We’ve included links to resources on Net Present Value (NPV) and the Internal Rate of Return (IRR) which you’re encouraged to peruse if you often make long-term investment decisions.

Direct and indirect costs

Some investments are not as simple as buying a new piece of equipment. They may require continuous maintenance and other costs that could impact your return on investment (ROI).

Let’s say your team has asked you to install a vending machine in the lab so they can replenish themselves without walking to the Starbucks across the street.

You estimate that your team will spend $2,000/month on snacks from the machine.

After the one-off fixed, direct cost to install the machine, you expect to incur the following recurring costs:

- $1,500/month rent

- $1,000/month inventory (snacks)

- $250/month waste management

Should you go ahead with the purchase?

At first sight, you’d be losing $2,000 - $2,750 = $750 per month on this investment, but some of these costs are, in fact, irrelevant and should not be included in your consideration.

One way to determine if a cost is indirect, and therefore irrelevant, is to see if it can be avoided by eliminating the cost object (in this case, the vending machine).

If nobody came to the lab for a month, what costs would be avoided?

❌ Rent — Fixed, Indirect — Rent for the room does not change from hosting the vending machine ✅ Inventory — Variable, Direct — You wouldn’t spend any money on snacks that month ❌ Waste management — Variable, Indirect — Waste costs would go down, but not to zero

The only recurring cost directly traceable to the vending machine is inventory, so after the payback period on the purchase of the machine, you’ll in fact be turning a profit of $2,000 - $1,000 = $1,000.

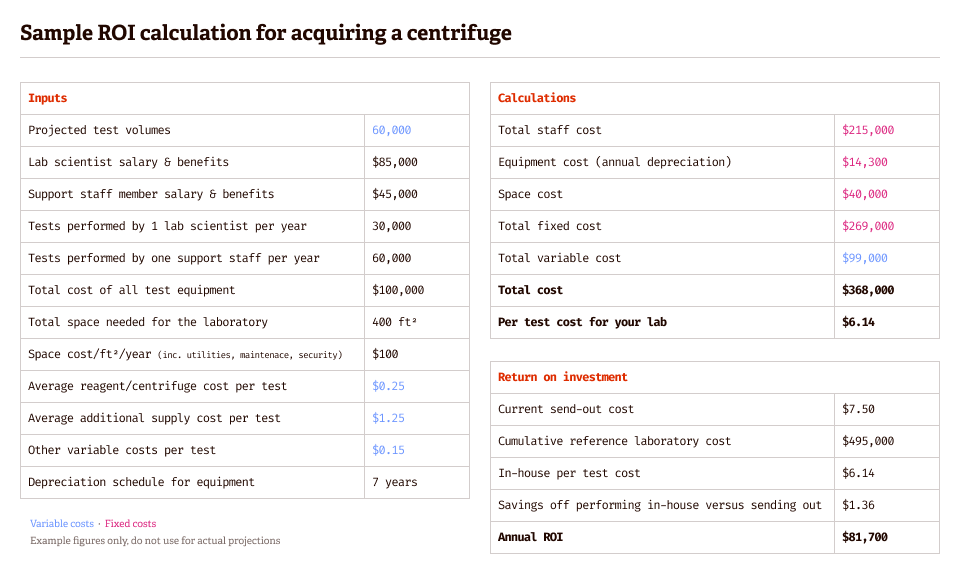

Here’s a more complex, practical example considering the return on investment (ROI) in a new centrifuge instead of outsourcing the tests:

Sunk costs

One other cost type that should not be taken into consideration in your decision-making are sunk costs, which are unavoidable costs that have already been incurred.

For example, the fact you already gave away $1,000 worth of Starbucks gift cards to all your staff is irrelevant, as that cost cannot be recovered.

Opportunity costs

On the other hand, you should consider what else you could have achieved with the same resources if you did not make this investment.

In the case of the vending machine, what if you used the empty room for a ping pong table or spent the cash to upgrade the office computer instead?

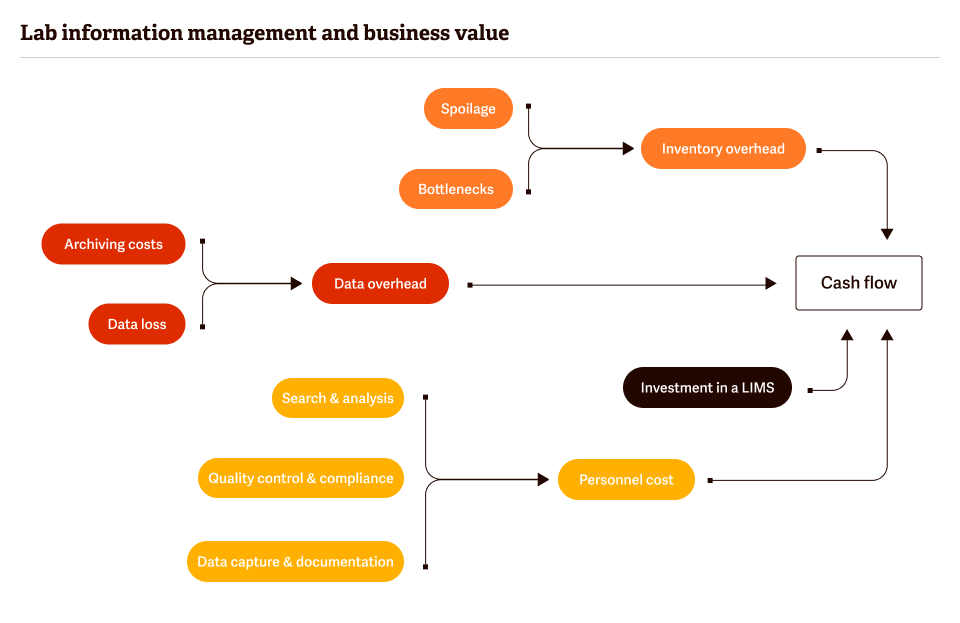

Business case for a LIMS

Time for a practical example to review what we’ve learned, and add a powerful new forecasting tool to your belt!

Imagine you’re a food science lab that just raised funding to accelerate its already rapid growth.

To increase your research throughput, you’re evaluating a Laboratory Information Management System (LIMS).

You’ve gone through the vendor’s proposal, and your team is excited about the product, but then comes the sticker shock — $120,000 per year!

Suddenly, the benefits become less clear, and your team becomes hesitant about the investment.

Should you go ahead with the upgrade?

A good place to start is to map out all the uncertainties that lead to business value. We can then use them to compare two scenarios, LIMS and the status quo.

Now that we have the parameters, we need to quantify or at least estimate each under both scenarios. How much will a LIMS accelerate documentation? How much will inventory waste be reduced?

If you can’t come up with an exact number (BINOCS is a powerful tool to collect the necessary data), try to find a minimum-maximum range from conversations with your team or with outside experts.

🐼 Soft benefits (and costs) Needless to say, not all benefits can be described in financial terms. For example, switching to an Electronic Lab Notebook can have effects on operating efficiency, employee morale, sales, and customer satisfaction. You should include these in your business case, but generally prioritize hard benefits in your decision-making.

Once you’ve got the numbers, you can stick them into an Excel spreadsheet, or better yet, input the numbers into Causal. Causal is a free web app that lets you build advanced models with Monte Carlo simulations, yet it’s easier to use than a basic spreadsheet.

We’ve built a simple model for you, but we encourage you to duplicate it and play around with the inputs or add entirely new factors specific to your lab.

https://my.causal.app/models/69711

As it turns out, you make your money back within just one quarter!