Screen: Entity risk

Six risk domains

Every entity extracted from the evidence is screened across six domains:

| Domain | What it helps answer |

|---|---|

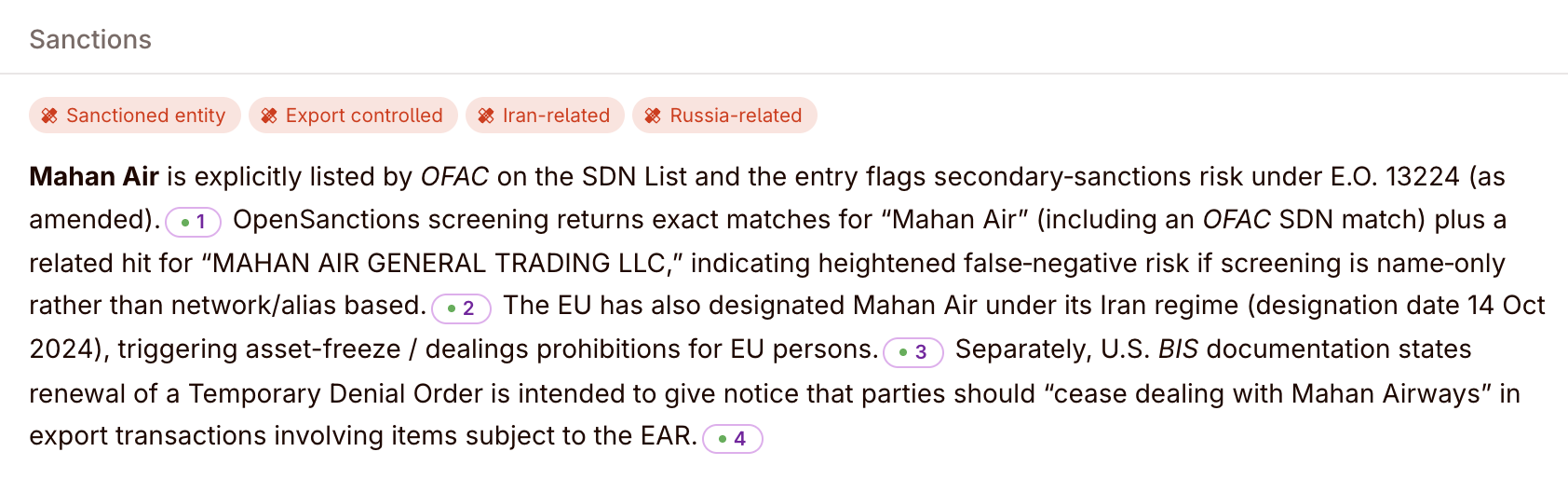

| Sanctions | Is this entity exposed to sanctions screening risk? Are there connections to sanctioned individuals, organisations, or jurisdictions? |

| PEP | Is a politically exposed person associated with this entity? Does that association create regulatory or reputational risk? |

| Litigation | Is there active or historical litigation, claims, or enforcement actions involving this entity? |

| Adverse media | Are there negative media signals — fraud allegations, regulatory actions, executive misconduct — worth escalation? |

| IP | Are there IP-related signals — disputed patents, licensing conflicts, trade secret concerns — that require diligence follow-up? |

| Licences | Are regulated licences missing, expired, or problematic? Are there gaps between what the entity claims and what the records show? |

Risk verdicts are generated per entity per domain, giving you a structured view of where exposure sits across the deal perimeter.

What the screening is based on

Entity risk is not based on only one source.

Colabra combines two evidence layers for the same entity:

- Internal deal evidence from the uploaded documents where the entity appears

- External online screening and enrichment from sanctions/watchlist sources, litigation and adverse-media research, corporate registries, IP records, and license or permit databases where relevant

That means Colabra is not only reading your uploaded documents back to you. It is also checking the entity against external sources outside the data room.

Examples of the external side include:

- sanctions and watchlist checks

- litigation and adverse-media research

- politically exposed person screening

- corporate-registry enrichment, including cross-registry discovery and jurisdiction-specific company records

- IP and license or permit lookups where the entity and jurisdiction make those checks relevant

Corporate-registry data is especially important even though it is not labeled as its own risk domain here. It helps verify who the entity is, how it is registered, and whether the internal evidence matches what external registries say.

Screening matters when it changes the deal question

Real deal example: risk signal plus commercial exposure

A sanctions or litigation flag becomes much more important when the same entity is a key supplier, lender, shareholder, or counterparty in a material agreement. The entity screen is useful because it can be read alongside the rest of the deal record, not because it produces a label on its own.

Drilling into a flagged entity

When an entity shows risk signals, open it to review:

- Linked files — which documents reference this entity and how many evidence connections exist.

- Risk verdicts — the screening result for each applicable domain, with supporting detail and external basis.

- Relationship graph — how this entity connects to other entities in the deal through ownership, governance, commercial, or advisory relationships.

- Perimeter status — whether the entity is included in or excluded from the deal scope.

The evidence matters more than the label. A risk verdict is useful only when you can inspect both the internal source material and the external basis behind the screen. Colabra surfaces linked files, risk detail, and relationship context so you can make an informed judgement rather than relying on a screening score alone.

Cross-referencing entity risk with contract exposure

The most valuable use of entity screening is when it intersects with contract extraction.

If an entity is flagged for sanctions risk and also appears as a counterparty in a material contract with change-of-control provisions, that is a compound risk worth immediate attention. If a key supplier is flagged for adverse media and represents 20% of cost-of-goods, the commercial exposure amplifies the screening signal.

Use the entity view alongside the findings tab. The entity graph shows who is connected and how. The risk register shows what contractual or financial exposure exists. Together, they answer the question that matters: where does risk concentrate, and what is the potential impact on the deal?